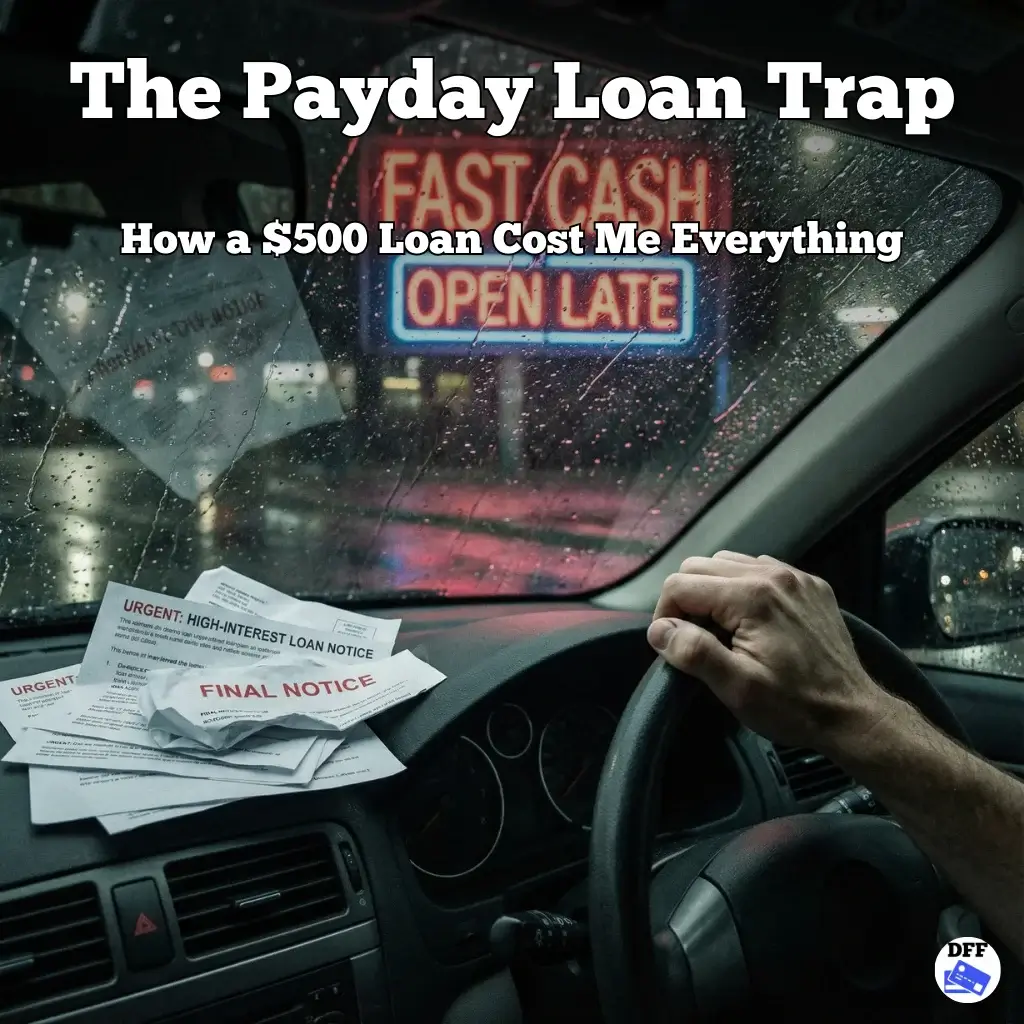

They call it “predatory lending” for a reason. They smell the blood in the water when you are desperate, and I was definitely desperate.

It happened last winter, on one of the coldest days of the year. My car’s transmission didn’t just die; it gave up the ghost in the middle of a busy intersection on a Tuesday morning. The mechanic quoted me exactly $500 to fix it so I could get to work. I checked my bank account three times, hoping the number would change, but it remained near zero. I had no emergency fund, my credit cards were maxed out, and I was too proud to call my parents and admit I was drowning.

That afternoon, I drove a rental past a storefront I had ignored a thousand times. It had a bright, buzzing neon sign that screamed “FAST CASH – NO CREDIT CHECK.” It felt like a lifeline thrown to a drowning man. I walked in. The air smelled like stale coffee and desperation. I signed a stack of papers without reading the fine print and walked out with the cash in less than twenty minutes. I told myself it was a one-time thing. I promised myself I would pay it back the second my paycheck hit in two weeks.

But when payday finally arrived, the math didn’t work. Life is expensive. After paying my rent, utilities, and groceries, I realized I didn’t have the full $500 plus the steep $75 fee to clear the balance. Panic set in. So, I did exactly what the friendly teller suggested with a smile: I “rolled it over.” I paid just the fee to extend the loan for another two weeks. It seemed harmless at the time, but I didn’t realize I was signing a contract with quicksand.

That was the trap. Two weeks turned into two months. Two months turned into six. Every single pay period, I was handing over massive chunks of my paycheck just to keep the loan afloat, never actually touching the principal balance. The interest rate was effectively over 400%. I was running on a hamster wheel, sweating and panicking, but getting absolutely nowhere.

The crushing weight of this payday loan debt started to consume my entire life. I stopped buying fresh groceries just to pay the fees. I started selling my clothes to consignment shops on weekends. I was working forty hours a week solely to pay a lender for a car repair that had happened half a year ago.

By the time I finally broke free, that simple $500 loan had cost me nearly $3,000 in fees and interest. The shame kept me trapped longer than the money did. I felt stupid for signing the contract, but I learned the hard way that these systems are designed to keep you poor.

Breaking the cycle required a moment of absolute humility. I finally broke down, crying at my kitchen table, and told my sister the truth about my payday loan debt. She didn’t judge me; she loaned me the lump sum to kill the snake once and for all, and I agreed to pay her back interest-free over time. Walking into that store to make the final payment was the most liberating moment of my life. I looked at that buzzing neon sign one last time and swore I would never, ever walk through those doors again.

The Lesson Learned

If you are staring at a broken car or an unexpected bill right now, please listen to me: sell something, work an extra shift, or ask for help, but do not take the quick cash. The relief lasts for twenty minutes; the nightmare can last for years.

The only way to protect yourself from these predators is to have your own safety net. Since that day, I have been aggressively building a $1,000 emergency fund. It is not a lot, but it is enough to ensure that the next time my transmission dies, I won’t have to sell my soul to fix it.

How do you build an emergency fund when you are broke? You can’t save money if you don’t know where it’s going. The secret is giving every dollar a job before the emergency happens. [Read our Guide on Zero-Based Budgeting] to start building your safety net today.

[…] – 01Dec2025 Credit Nightmares Regret buying a house Debt Confessions The Payday Loan Trap: How a $500 Loan Cost Me Everything […]

[…] already experienced enough stress with my finances—as I wrote about in my story regarding [“The Payday Loan Trap“]—and I wasn’t willing to risk a lawsuit just to pay a […]