It was a Tuesday evening. Tuesdays are supposed to be safe.

I was standing in the checkout line at my local grocery store. It was the busy hour, right after work. Behind me, a mother was wrestling with a toddler, and behind her, a businessman was checking his watch. The line was long.

My cart wasn’t even full. Just the essentials: milk, bread, eggs, some chicken, and a box of cereal. Total cost: $64.30.

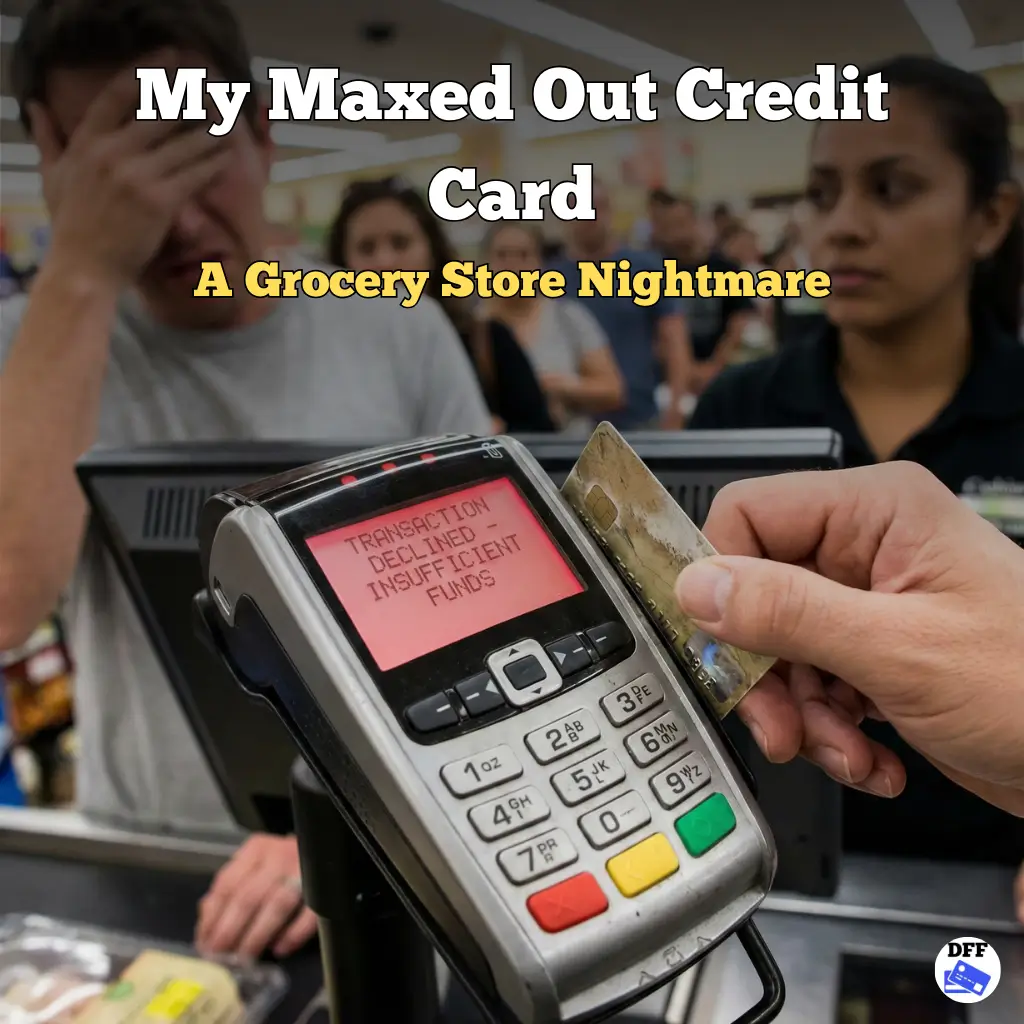

I smiled at the cashier, swiped my card, and waited for the familiar “beep” of approval. Instead, the machine made a harsh, buzzing sound. “DECLINED.”

My heart stopped. I felt the heat rise up my neck instantly. “Oh, that’s weird,” I lied, my voice cracking slightly. “It must be the chip. Let me try again.”

I swiped it again. “DECLINED.”

I knew exactly why. It wasn’t the chip. It wasn’t a bank error. It was a maxed out credit card. I had hit my limit of $3,000 three days ago, and I had been praying that maybe, just maybe, a pending payment had cleared to free up $70. It hadn’t.

The Walk of Shame

The cashier didn’t say anything at first. She just gave me that look—you know the one. It wasn’t mean, exactly, but it was tired. It was a mix of pity and “please don’t let this be a problem” annoyance. Then she asked the question I was dreading, loud enough for everyone to hear: “Do you have another form of payment?”

I opened my wallet, pretending to look for something I knew wasn’t there. My hands were actually shaking a little. I thumbed through old receipts and a punch card for a coffee shop, praying a twenty-dollar bill would magically materialize. But it was empty. No cash. My debit card was right there in the slot, but I couldn’t touch it because my checking account was already $30 overdrawn. It was just me and that useless piece of plastic.

“I… I don’t,” I whispered. My voice was so quiet I barely heard it myself.

The silence that followed felt heavy, like the air had been sucked out of the store. The businessman behind me shifted his weight and let out one of those loud, dramatic sighs—the kind that clearly says, “My time is more important than your crisis.” The mother with the toddler just stared at me, holding a box of crackers, probably wondering why I was holding up the line. I felt small. I felt like a child who had lost their mom.

I realized I had to do the unthinkable. I had to abandon the food.

“I’m sorry. I really am,” I mumbled, refusing to make eye contact. I backed away from the cart, leaving the bagged chicken and the milk sitting there on the conveyor belt like a sad little monument to my failure. I turned around and started walking. It was the longest walk of my life. I could feel the heat radiating off my face, and I swear I could feel every single pair of eyes burning into my back until the automatic doors finally slid open and let me out.

Why We Ignore the Limit

Here is the truth that’s hard to admit: having a maxed-out credit card doesn’t happen overnight. It’s not like I went out and bought a boat or a diamond necklace. It is a slow, creeping disaster that sneaks up on you five dollars at a time.

For months, I had been treating my credit limit like a target instead of a ceiling.

When the limit was $1,000, I spent $990. Then, the bank sent me a letter saying, “Congratulations! You’ve earned an increase!” and bumped me to $3,000. Did I save that extra buffer? No. I treated it like a raise. Within two months, my balance was sitting at $2,950.

I was playing a dangerous game called “Living on the Edge.” I kept lying to myself, thinking, “I’m fine. As long as I can afford the minimum payment, I’m winning.” But I wasn’t winning. I was drowning in slow motion.

When you live with a maxed-out card, you have absolutely zero margin for error. You are walking a tightrope across the Grand Canyon without a safety net, just praying the wind doesn’t blow. And that Tuesday at the grocery store? That was the wind blowing. That was me finally falling off.

The Crying in the Car Moment

I got to my car, sat in the driver’s seat, and burst into tears. It wasn’t about the milk or the eggs. It was about the loss of dignity.

I was a working adult. I had a job. And yet, I couldn’t buy $64 worth of food. I pulled up my banking app and stared at the red numbers. Balance: $3,012.45 / Limit: $3,000.00

That over-limit fee was the cherry on top. I realized then that I had been lying to myself. I wasn’t “managing” my finances. I was in a crisis.

Turning Humiliation into Fuel

That humiliation was the best thing that ever happened to me. If the card had gone through, I would have bought the groceries, gone home, and continued digging my hole deeper.

The shame of that decline forced me to face reality. I went home that night and finally told my partner the truth about our debt. We cut up the maxed out credit card that very evening. We literally took scissors to it on the kitchen table.

It was scary to not have that “backup,” but I realized that the card wasn’t a backup—it was an anchor dragging me down.

Conclusion

If you are reading this with a card that is dangerously close to its limit, please listen to me: Stop. Don’t wait for the cashier to tell you “Declined.” Don’t wait for the public humiliation.

A maxed out credit card is not a financial tool; it is an emergency siren. Cut it up. Switch to cash. Do whatever you have to do to regain your dignity. Because being able to buy milk without a panic attack? That is true freedom.

Have you ever had a card declined in public? How did you handle the embarrassment? Share your story below—you are definitely not alone.

My grocery store nightmare was just one chapter of my journey. You are not alone in this fight. Read more real-life Debt free stories to remind yourself that financial freedom is possible.

[…] – 17Dec2025 Debt Confessions How Spending Money on Mobile Games Ruined My Finances Credit Nightmares My Maxed Out Credit Card: A Grocery Store Nightmare […]