It happened on a Tuesday. Tuesdays are supposed to be boring, predictable days, but this particular Tuesday felt like the universe was testing my resolve.

I was three months into my debt-free journey. I was motivated. I was intense. I had been throwing every single spare dollar at my credit card balance like my life depended on it. I was eating rice and beans, saying “no” to happy hours, and feeling incredibly proud that I had lowered my balance by $800.

Then, I turned the key in my ignition. The engine coughed, sputtered, and died.

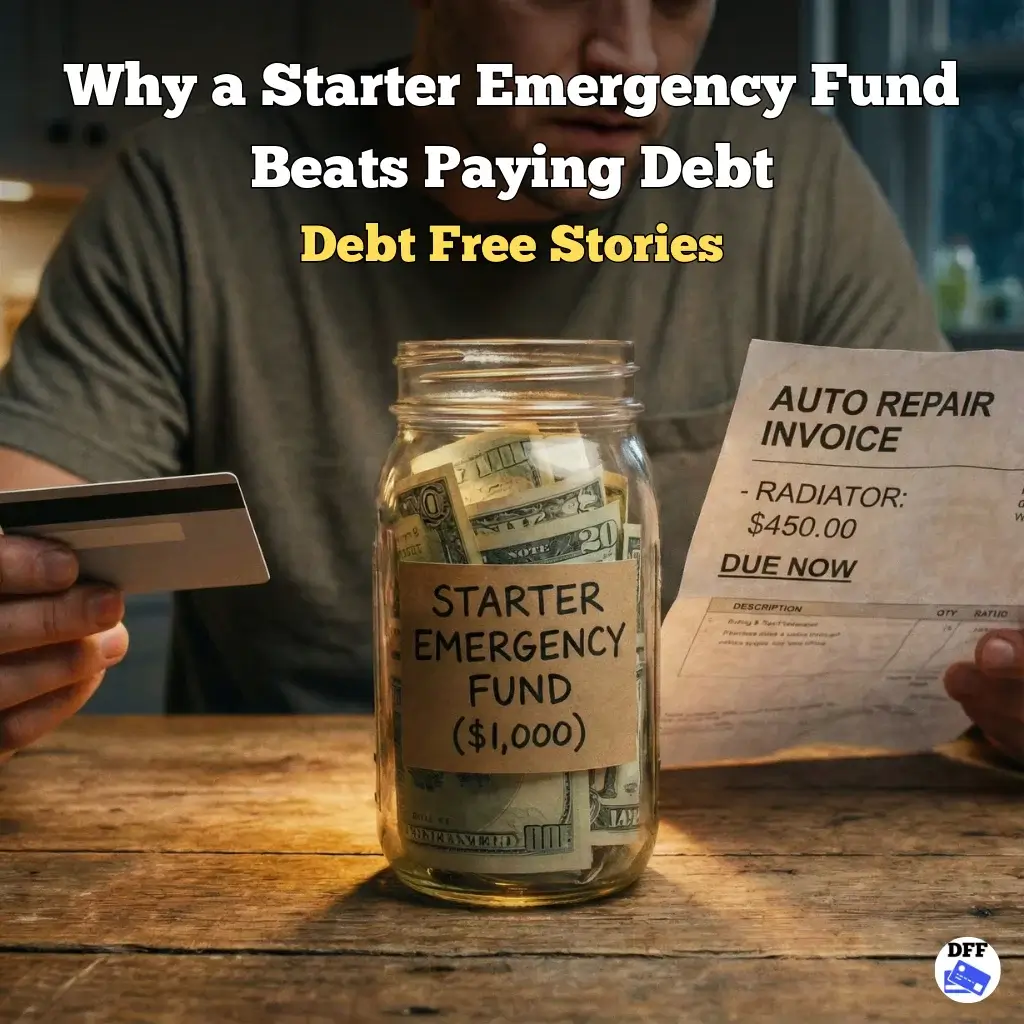

The mechanic gave me the news: a cracked radiator. The cost? $450.

My stomach dropped. I checked my bank account app, even though I already knew the answer. Balance: $32.40.

I had sent all my money to the credit card company three days earlier. I had no choice. With a heavy sense of defeat, I pulled out the very same credit card I was trying to pay off and swiped it. In three seconds, half of the progress I had made over the last three months was wiped out.

I drove home feeling like a failure. I felt like a hamster on a wheel—running as fast as I could but going absolutely nowhere.

That was the moment I realized the hard truth: You cannot get out of debt if you don’t have a buffer. This is why building a starter emergency fund isn’t just a “nice to have”—it is the single most critical step in your financial survival.

The Math vs. The Reality

If you talk to a purely logical financial advisor, they might tell you that saving cash while in debt is a mistake.

Mathematically, they are right. It makes zero sense to have $1,000 sitting in a savings account earning 0.1% interest while you have a Visa card charging you 24% interest. You are losing money on the spread.

But here is what I learned after that radiator incident: Personal finance is 80% behavior and only 20% head knowledge.

If you focus only on the math, you strip away the human element of risk. When I sent all my cash to the debt, I left myself exposed. I was walking on a tightrope without a net. The moment the wind blew (a broken car, a sick pet, a medical copay), I fell right back into the hole.

To break this cycle, I had to stop looking at the interest rates and start looking at my behavior. I needed a financial safety net more than I needed to save a few dollars in interest.

The Cycle of Borrowing

The reason so many of us stay in debt for years isn’t that we don’t make enough money; it is that we can’t stop borrowing.

Every time an unexpected expense pops up, we reach for the plastic. It’s a reflex. If you want to know how to stop using credit cards for good, the answer is not willpower. It’s liquidity. You need access to cash that is strictly reserved for when life punches you in the face.

That is the sole purpose of a starter emergency fund. It is typically $1,000 (or one month of expenses if your income is very unstable) set aside before you start aggressively attacking your debt.

It stands between you and the credit card companies. It is your insurance policy against Murphy’s Law.

How to Start an Emergency Fund With No Money

When I decided to build my fund, I faced a glaring problem: I was broke. After paying minimum payments and basic living expenses, I had nothing left.

If you are wondering how to start an emergency fund with no money, you have to get radical. You have to realize that this is an emergency. Your house is on fire.

Here is exactly how I scraped together my first $1,000 in less than 30 days:

- I Paused the Snowball: This was painful. I stopped making extra payments on my debt. I only paid the minimums. Every extra dollar went into a separate savings account.

- I Sold the Clutter: I walked through my house with a laundry basket and filled it with things I didn’t need. Old video games, designer purses I couldn’t afford, and kitchen gadgets I never used. I listed them on Facebook Marketplace and eBay. That weekend alone, I made $300.

- The “No Spend” Sprint: We had just finished a “No Spend Month” (you can read my full story on that in the previous post), but I kept the intensity going. No eating out. No coffee shops. No subscriptions.

- I Hunted for Found Money: I checked unclaimed property sites, rolled loose change, and even returned a pair of shoes I had bought but never wore.

The Peace of Mind is Priceless

It took me about four weeks to hit $1,000. When I saw that comma in my bank account, something in my brain shifted.

I wasn’t rich. I still had thousands of dollars in debt. But for the first time in my adult life, I wasn’t afraid of the phone ringing. I wasn’t terrified of the “Check Engine” light.

Two months later, my dog needed an emergency vet visit. The bill was $250. In the past, that would have ruined my week. I would have panicked.

This time? I simply transferred the money from my starter emergency fund to my checking account and paid with a debit card. No interest. No new debt. No shame.

It turned a financial crisis into a mere inconvenience.

That $1,000 didn’t just sit in the bank; it bought me my dignity back. It gave me the solid ground I needed to finally stand up, cut up the credit cards, and attack my debt for real—this time, without looking back.

Building this safety net was one of the smartest financial moves I ever made. But I haven’t always made smart moves. In fact, I made a massive mistake that cost me thousands and taught me a painful lesson about high-pressure sales. Want to see what not to do? Read my confession here: Regret Buying a Timeshare: My Story

[…] – 13Dec2025 Credit Nightmares The $2,000 Free T-Shirt: Real Money Stories for Adolescents Exit Strategies Why a Starter Emergency Fund Beats Paying Debt […]

[…] [Read: Why a Starter Emergency Fund Beats Paying Debt] […]